As parents of two young children, we find ourselves squarely in the crosshairs of university marketing departments nationwide. With a significant sum, over $800,000, diligently saved across two 529 plans, our objective is clear: to cover the full cost of higher education for our children in the coming 9 to 12 years. We recognize that without exceptional academic prowess or extraordinary circumstances, full tuition payment is our reality, a consequence of earning above the threshold for substantial financial aid or subsidized tuition. This financial commitment, substantial as it is, compels a rigorous examination of the return on investment offered by higher education, much like any other significant purchase we make – from automobiles and electronics to homes and vacations.

The fundamental value proposition of a college degree is undergoing a profound transformation, accelerated by the rapid advancements in Artificial Intelligence and the ubiquitous availability of information online. The traditional four-year degree, once a cornerstone of professional preparation, now appears increasingly anachronistic in an era where knowledge acquisition has been dramatically expedited by technology. A streamlined, three-year path to graduation seems a more logical and efficient model, reflecting the current pace of technological and societal change.

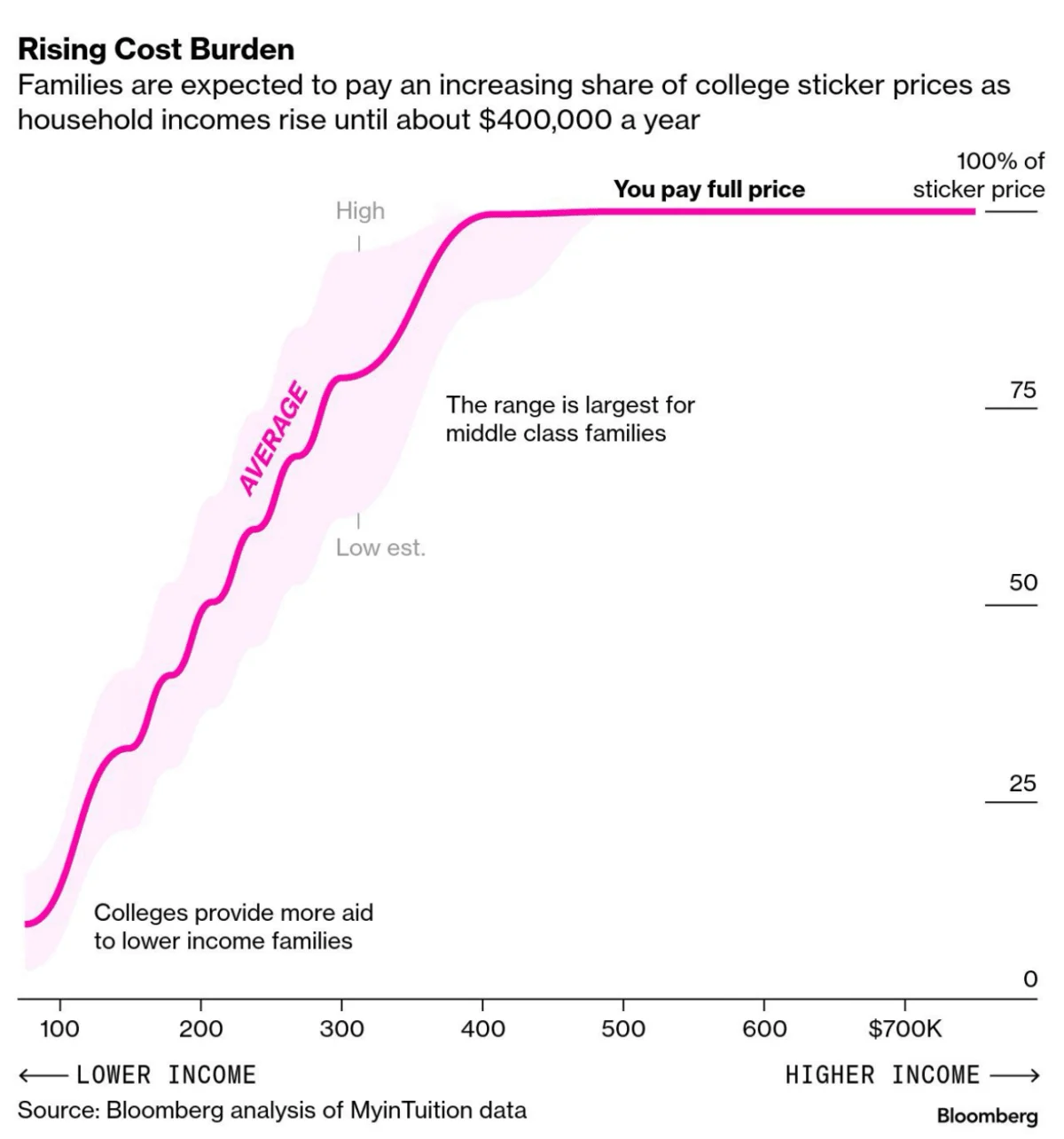

Compounding this evolving value is the persistent, often unchecked, rise in tuition fees, consistently outpacing inflation. This trend is particularly perplexing when juxtaposed with the stated mission of many educational institutions: to cultivate young minds and equip them for the future. If accessibility and preparedness are genuine priorities, a reduction in tuition would logically serve to broaden access for a greater number of families, rather than restricting it. Furthermore, esteemed universities, particularly those with acceptance rates below 20%, could consider strategically expanding their class sizes to meet demand. Such an expansion, if carefully managed, could enhance their mission of educating a wider student population without necessarily diluting the quality of education.

A critical missing piece in the current higher education landscape is accountability. Why do colleges not offer guarantees on a minimum employment income for their graduates? A willingness to stand behind the quality of their education with such a guarantee would serve as a powerful testament to their confidence in the programs they offer and the skills they impart.

The inertia within the higher education system is not an enigma; it is rooted in the fundamental operational realities of these institutions. Whether classified as non-profit or for-profit, universities function as businesses with the imperative to maintain solvency. Lowering tuition directly impacts operating budgets, as does reducing the enrollment of international students who often contribute significantly to tuition revenue. Expanding class sizes, while potentially increasing accessibility, can be perceived as diluting the exclusivity and prestige associated with certain institutions. The notion of guaranteeing graduate employment income, however, presents a risk that most institutions are unwilling to undertake, signaling a potential lack of confidence in the tangible outcomes of their educational offerings. In essence, universities, like any business, are driven by the need to remain competitive and avoid the risk of failure.

For parents, the pursuit of a college education for their children often necessitates significant personal sacrifice. Many are compelled to deplete retirement savings and extend their working careers in jobs they may not find fulfilling, all to meet the escalating costs of tuition. This financial strain is a palpable reality, leading to deferred personal gratification and a persistent focus on future financial obligations. The specter of a child facing diminished career prospects due to a lack of a degree, particularly in the face of rapid AI-driven automation, adds another layer of anxiety. The irony is stark: after dedicating over two decades to formal education, from early childhood through college, graduates may still find themselves underemployed or struggling to find employment, a consequence of rapidly evolving job markets and advice that can quickly become obsolete.

The pressure on students to excel academically and extracurricularly from an early age, to gain admission to competitive institutions, is immense. This often leads to a pragmatic pivot in career aspirations towards fields with perceived higher earning potential, such as technology, consulting, or finance, even if these deviate from original passions. This pursuit of financial security and prestige can, in turn, lead to careers that lack personal fulfillment, trapping individuals in a cycle of working for financial gain rather than passion, and potentially perpetuating this cycle for their own children.

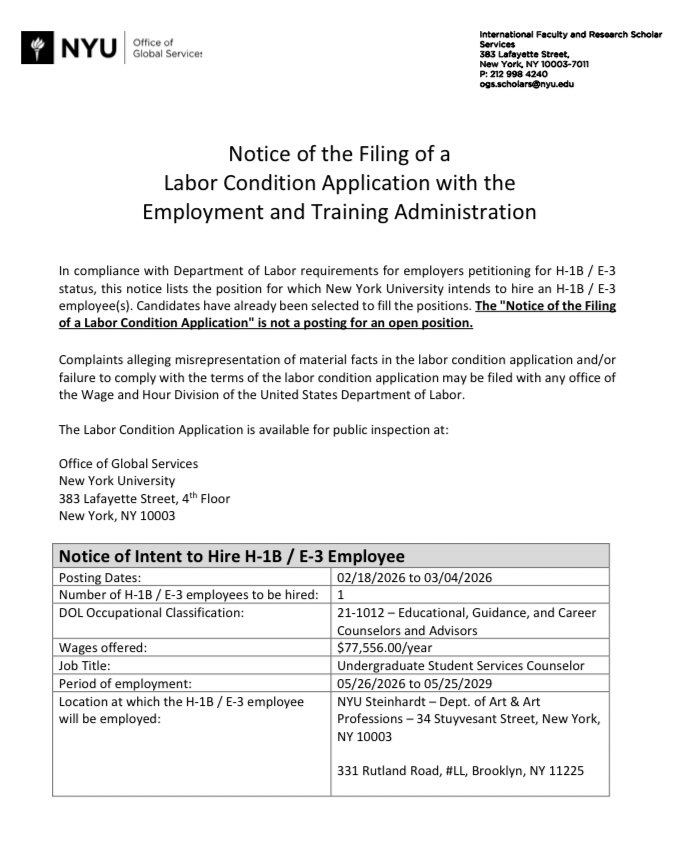

A concerning trend has emerged with reports from independent journalists highlighting universities posting job openings that appear to preferentially target H-1B visa holders, rather than prioritizing domestic graduate pools. While international diversity is a valuable asset, the question arises: where are the opportunities for American graduates? This practice raises concerns about whether institutions are creating pathways for international students or whether a genuine lack of qualified American candidates exists, despite universities offering degrees in these very fields. For prospective students and their families investing heavily in higher education, understanding a university’s hiring practices becomes a crucial part of due diligence.

For instance, the University of Virginia (UVA) reportedly hired an H-1B worker for a Data Analyst position with a salary of $80,576. This occurred despite UVA’s School of Data Science graduating a substantial number of students annually, alongside a larger undergraduate population. The implication that thousands of graduates, including hundreds specifically trained in data science, could not fill this single role, or that no recent graduates were willing to accept it, warrants scrutiny. While the pursuit of talent is a universal objective, American universities, especially those receiving public funding, should arguably place a greater emphasis on supporting and prioritizing their domestic student body. If institutions are indeed focused on supporting their international alumni, this should be transparently communicated. However, for any prospective student, particularly those from out of state paying higher tuition, such hiring patterns serve as a potential red flag regarding the quality of education and the institution’s commitment to its own graduates.

In a labor market where college graduates already face challenges in securing employment, and with AI accelerating the displacement of knowledge workers, universities would logically be expected to exert maximum effort in placing their own graduates. Publicly advertising for H-1B visa holders for roles that could ostensibly be filled by domestic talent sends a contradictory message. It suggests that American graduates may not be considered sufficiently qualified for these positions, a conclusion that prospective students and parents must weigh carefully when considering the substantial investment of time and financial resources. The cost extends beyond tuition; it encompasses four years of a student’s life and the opportunity cost of alternative paths. The prospect of investing heavily in an education only for one’s child to be overlooked for job opportunities due to their nationality is a deeply concerning implication.

A more cynical explanation for this hiring trend is the pursuit of cost savings. Universities may opt to hire foreign workers at potentially lower wage rates than what might be required for American workers, thereby reducing operational expenses. While companies in the private sector may engage in such practices to enhance profit margins, the mission of educational institutions, particularly those receiving public funds, should arguably extend beyond pure financial optimization to encompass the development and support of their domestic student population.

Navigating the complex landscape of college selection and financing requires a strategic approach. Families are advised to adhere to a "one-fifth rule" for net tuition costs, ensuring that the annual net tuition per child does not exceed one-fifth of the gross household income, with a preference for one-seventh or less. This metric serves as an initial filter, preventing financially imprudent decisions. The focus should always be on the net cost after all grants, scholarships, and financial aid, rather than the published sticker price. Utilizing the Net Price Calculator provided by accredited universities is an essential step in this process.

Furthermore, a thorough investigation into graduate employment outcomes, disaggregated by major, is crucial. The success of a computer science degree from a robust state university might significantly outperform a humanities degree from a prestigious private institution. Examining median starting salaries and employment rates for specific departments, rather than generalizing across the entire university, provides a more accurate picture of return on investment.

Crucially, families should scrutinize the actual practices of institutions, not just their stated missions. The prevalence of H-1B hiring for roles that could be filled by domestic graduates is a significant indicator. If a university appears to prioritize foreign hires over its own alumni, it may suggest a lack of confidence in its graduates’ qualifications or a diminished commitment to their post-graduation success. Prospective students have the right to inquire about these hiring policies before making a substantial financial and temporal commitment.

The debt-to-income ratio at graduation is another vital consideration. A prudent guideline suggests that total student loan debt should not exceed the expected first-year salary in the chosen field. If this ratio is unfavorable, the institution may be too expensive for that particular career path. Exploring community college and transfer pathways can also offer substantial cost savings, potentially cutting the overall cost of a degree by 40-50% while still yielding a comparable diploma.

Financing higher education without jeopardizing personal financial security requires careful planning. Establishing a 529 plan early and contributing consistently is paramount, leveraging tax-advantaged growth. The flexibility to roll over unused funds into a Roth IRA provides an additional layer of security. However, the cardinal rule remains: do not sacrifice retirement savings for college expenses. Retirement cannot be funded through loans, whereas college costs can be partially financed through borrowing. Prioritizing retirement security ensures a stronger financial foundation for both parents and, by extension, their children.

Even if families believe they may not qualify for financial aid, applying is essential. Forms like the FAFSA and CSS Profile are gateways to grants, scholarships, and subsidized loans. Many families forgo this step based on assumptions about their income, thereby missing out on significant financial support. Research indicates that households earning substantial incomes can still qualify for aid, underscoring the importance of completing these applications.

An open and honest conversation with children about the financial realities of college is indispensable. Students should understand the total cost, the family’s contribution, and their projected debt burden. This transparency fosters informed decision-making and a greater sense of ownership over the educational journey. For students who may not be in a position to secure substantial merit-based aid, a realistic assessment of college choices is necessary to avoid undue financial strain.

Looking ahead, the hope is that by the time current young children reach college age, the higher education landscape will have evolved. Ideally, a traditional four-year degree will no longer be the sole prerequisite for success, allowing significant 529 plan savings to be redirected towards more direct forms of adult launch support. The race between technological advancement and the adaptation of traditional education is a slow one, and societal pressure to pursue a four-year degree may persist even as its economic justification erodes.

The aspiration is for universities to prioritize hiring their own American graduates, fostering a reciprocal relationship between institution and alumnus. Increased tuition assistance that doesn’t necessitate parental financial ruin is also a critical need. Ultimately, a more widespread adoption of rigorous financial analysis before committing to college expenses is essential.

The current disruption of knowledge work by AI poses an existential challenge to institutions primarily engaged in knowledge provision. The stakes for making a poor college decision have never been higher. Thorough research, diligent financial assessment, and demanding that institutions demonstrate tangible value are imperative before committing substantial financial resources and years of a student’s life.

The increasing trend of universities posting jobs for H-1B visa holders instead of their own American graduates raises critical questions for prospective students and their families. The underlying rationale behind this practice, whether it stems from a perceived lack of qualified domestic candidates or a strategic cost-saving measure, has profound implications for the perceived value and accessibility of higher education. As the cost of college continues to escalate, and the job market evolves at an unprecedented pace, parents and students must engage in a more critical and informed decision-making process, demanding greater accountability and demonstrable value from educational institutions.

Navigating the complexities of college financing is significantly aided by a clear understanding of one’s financial standing. Comprehensive financial tracking, encompassing net worth, asset allocation, income generation, and investment returns, empowers families to make informed decisions about affordability. Utilizing free financial tools can provide the necessary clarity to confidently allocate resources towards one of the most significant investments a family can make.