The financial markets, often characterized by periods of intense volatility, present unique challenges and opportunities for investors. In recent years, geopolitical instability and economic shifts have led to significant market downturns, prompting many parents to re-evaluate their investment strategies, particularly concerning their children’s financial future. For many, the instinct during such times is to protect assets. However, for some, a more proactive and defiant approach emerges: strategically investing more than the annual gift tax exclusion limit into their children’s custodial accounts. This strategy, while seemingly complex due to tax implications, offers a powerful way to leverage market dips for long-term generational wealth building, provided a clear understanding of the relevant tax regulations is in place.

Understanding the Gift Tax Exclusion: More Than Just a Limit

At the core of this strategy lies the annual gift tax exclusion. For 2024, this limit is set at $18,000 per recipient. This means an individual can gift up to this amount to another person each year without incurring any gift tax liability or needing to report the gift to the Internal Revenue Service (IRS). It’s crucial to distinguish between "reporting" and "paying" taxes. Exceeding the annual exclusion does not automatically trigger a tax payment. Instead, it necessitates the filing of IRS Form 709, United States Gift and Generation-Skipping Transfer Tax Return. This form serves as a disclosure to the IRS that a gift exceeding the annual limit has been made. The amount gifted beyond the annual exclusion is then deducted from the donor’s lifetime gift tax exclusion.

The lifetime gift tax exclusion is a substantial safety net. For 2024, it stands at $13.61 million per individual, with provisions for married couples to combine their exclusions for a total of $27.22 million. This exceptionally high threshold means that very few individuals will ever exhaust their lifetime exemption. The vast majority of Americans gifting assets to their children will not face actual gift tax payments. Their excess contributions simply reduce their available lifetime exemption. For instance, gifting $30,000 to a child when the annual exclusion is $19,000 means $11,000 counts against the lifetime exemption. This is a relatively small reduction from a $15 million (or higher) total exemption, representing a minimal impact on the overall estate planning capacity.

The Filing Requirement: Form 709 Explained

When an individual surpasses the annual gift tax exclusion for a given recipient, filing Form 709 becomes a necessary step. This form is due by April 15 of the year following the gift. For example, gifts made in 2024 that exceed the annual exclusion would require Form 709 to be filed by April 15, 2025. Extensions are available, typically mirroring extensions for income tax filings. The process involves detailing the gift, calculating the amount that exceeds the annual limit, and specifying how much of the lifetime exemption is being utilized.

For those utilizing tax preparation software or working with a Certified Public Accountant (CPA), incorporating Form 709 is generally a straightforward process. Most tax professionals are accustomed to handling these filings. It is important to note that married couples can combine their annual exclusions. In 2024, a married couple can collectively gift up to $36,000 ($18,000 per spouse) to a single recipient without needing to file Form 709. This "gift splitting" strategy can significantly increase the amount that can be transferred without triggering the filing requirement.

The Consequences of Non-Compliance: Penalties and Statute of Limitations

Failure to file Form 709 when required can lead to penalties. However, the nature and severity of these penalties are often misunderstood. If no gift tax is actually owed—which is the case for most individuals given the high lifetime exemption—the financial penalty for failing to file is typically zero. The IRS penalties for failure to file are calculated as a percentage of the unpaid tax, not the gift amount itself. If the tax due is $0, the penalties also calculate to $0.

Despite the lack of a direct financial penalty in many scenarios, not filing Form 709 carries significant long-term implications. The filing of Form 709 initiates a three-year statute of limitations for the IRS to audit the reported gift. If the form is never filed, this statute of limitations never begins to run. This means the IRS could, theoretically, audit past gifts at any point in the future, even decades later. For estate planning purposes, this open-ended audit risk can create considerable complications and stress for heirs and estate administrators, particularly if the original donor is no longer available to provide clarification. Maintaining meticulous records and timely filing ensures a clear and documented gift history, providing closure and minimizing potential future liabilities.

How the IRS Identifies Exceeding the Limit

The question of how the IRS becomes aware of gifts exceeding the annual exclusion is often a point of curiosity. For cash transfers into custodial brokerage accounts, the IRS generally relies on the taxpayer’s voluntary disclosure via Form 709. Brokerage firms do not typically report individual deposit amounts into custodial accounts to the IRS for gift tax compliance purposes. While banks are required to file Currency Transaction Reports (CTRs) for cash deposits exceeding $10,000, these reports are primarily aimed at combating money laundering and are not directly linked to gift tax reporting. Similarly, wire transfers or ACH transfers between an individual’s own accounts or to a child’s account do not automatically trigger an IRS gift tax inquiry. The gift tax system, to a significant extent, operates on a self-reporting basis, with the expectation that taxpayers will comply with their obligations. The IRS’s primary mechanism for identifying unreported large gifts often occurs during the estate tax audit process after an individual’s death.

The Practical Relevance for Most Investors

For the vast majority of individuals, especially those whose projected estates will fall below the lifetime estate tax exemption threshold (currently $13.61 million per person in 2024), exceeding the annual gift tax exclusion may seem inconsequential. Since the annual and lifetime exemptions are part of a unified system, exceeding the annual limit simply means utilizing a portion of the lifetime exemption. If an individual’s estate is unlikely to approach the lifetime exemption limit, the act of filing Form 709 becomes largely an administrative exercise, ensuring proper documentation without any immediate tax cost.

However, this perspective can shift if future legislative changes significantly alter estate tax laws. Historically, there have been proposals to reduce the lifetime exemption considerably. Should such changes occur, previously reported gifts would factor into the calculation of the taxable estate. Therefore, maintaining accurate records and timely filing of Form 709, even when no tax is immediately due, offers a prudent long-term strategy for managing potential future estate tax liabilities and providing clarity for heirs.

Strategic Investment During Market Downturns: A Parental Imperative

The decision to invest more than the annual gift tax exclusion during a market downturn is often driven by more than just tax efficiency; it is frequently an emotional and strategic response to perceived opportunity. During periods of market decline, the cost basis of investments decreases, allowing for the acquisition of more shares at a lower price. For parents focused on long-term wealth building for their children, this presents a compelling opportunity to "buy low" within tax-advantaged custodial accounts.

The underlying philosophy is one of active engagement with the market, rather than passive observation. When portfolios decline, it can feel disempowering. However, for those with the financial capacity and a long-term investment horizon, deploying capital during such times can be a highly effective wealth-building strategy. The principle of "front-loading" investments—contributing larger amounts earlier in an investment lifecycle—allows compounding to work more effectively over time.

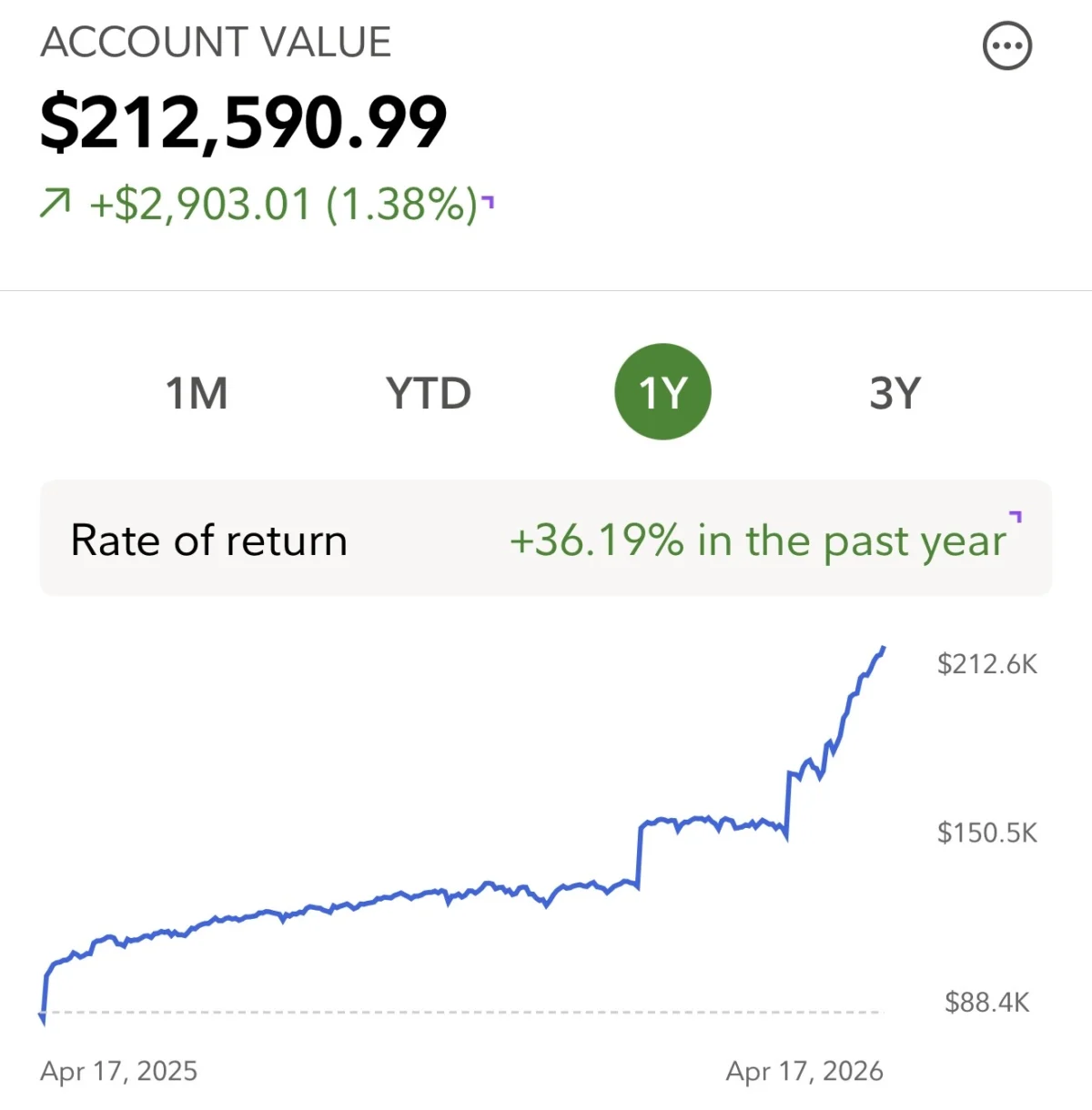

A $500,000 Custodial Account Goal: Modeling the Path

To illustrate the impact of this strategy, consider a goal of accumulating $500,000 in each child’s custodial investment account by the time they graduate college, around age 23. For children aged 6 and 9, with existing balances of approximately $135,000 each at the beginning of 2026, the time horizon for compounding is significant. Assuming a conservative average annual return of 7%—a reasonable expectation for a diversified equity portfolio and below the historical average of major market indices like the S&P 500—the required annual contributions become manageable.

For the older child, with approximately 17 years until college graduation, the projected annual contribution needed to reach the $500,000 target is around $9,400. This amount falls comfortably within the $18,000 annual gift tax exclusion, meaning no Form 709 would be required. The younger child, with an additional three years for compounding, would require an even lower annual contribution, approximately $6,700, highlighting the power of extended time horizons in investment growth.

The significant existing balance of $135,000 plays a crucial role. Projections indicate that more than half of the $500,000 target will be generated by the growth of capital already invested, rather than future contributions. This underscores the immense value of early and consistent investment, especially during periods of market appreciation and subsequent recovery.

Front-Loading as a Strategic Advantage

The act of investing $30,000 per child, exceeding the $19,000 annual exclusion, can be reframed as strategic "front-loading." By investing at a time when asset prices are depressed, parents are effectively purchasing future growth at a discount. Each market recovery, represented by an upward tick in stock indices, signifies a missed opportunity if capital is not deployed. This aggressive approach is not about timing the market perfectly but about capitalizing on moments of market dislocation to enhance long-term compounding for the benefit of the next generation.

The ultimate goal is not to achieve an exact financial target, as market returns are inherently variable. Instead, it is about establishing and adhering to a disciplined investment system: consistent contributions, investment in low-cost index funds, resilience during market downturns, and strategic deployment of capital during opportune moments. This disciplined approach, akin to consistently maximizing contributions to a 401(k) plan, can yield substantial results over a decade or more.

The Purpose and Nuance of Gift Tax Rules

The gift tax framework was primarily established to prevent the evasion of estate taxes through the intergenerational transfer of vast fortunes. It was not designed to penalize parents who, during a market downturn, make more substantial gifts to their children to capitalize on investment opportunities. The existence of a substantial lifetime exemption reflects a legislative intent to facilitate generational wealth transfer for ordinary families.

Therefore, parents considering exceeding the $18,000 annual exclusion for their children during a market dip should not be deterred by the term "gift tax." The administrative burden of filing Form 709 is minimal compared to the potential financial benefit of acquiring assets at a discount within accounts designed for long-term growth. The strategic advantage of investing aggressively for children, especially when they have decades of compounding ahead, is often a compelling reason to navigate the manageable paperwork associated with exceeding the annual exclusion.

Optimizing Personal Finances for Generational Wealth Transfer

Before embarking on aggressive gifting strategies, it is paramount for individuals to ensure their own financial house is in order. A comprehensive understanding of one’s own net worth, cash flow, and investment performance is essential for effective long-term financial planning. Tools that aggregate financial accounts and provide a holistic view can be invaluable. For example, platforms offering free financial tracking and analysis can help identify areas for optimization, such as hidden fees, suboptimal asset allocation, or tax inefficiencies.

Seeking a second opinion from a financial professional can also uncover blind spots and missed opportunities. This proactive approach to personal financial management not only strengthens an individual’s own financial security but also provides a more robust foundation for their ability to gift and support future generations. Clarity and disciplined financial management are the cornerstones of successful wealth building, both for oneself and for the legacy one intends to leave.